{kind=link}

Before diving into the concept of why you need emergency funds, let us understand what an emergency fund is.

What is an emergency fund?

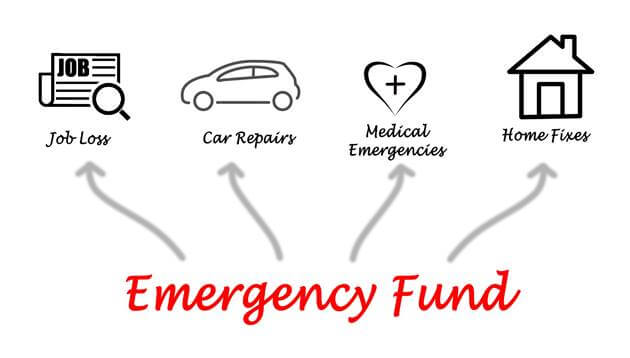

The fund has been kept aside as savings to provide financial protection during unexpected events. Unexpected events can be medical emergencies, job losses, house repairs, car repairs, losses due to speculation in the stock market, losses in business, etc.

Now let us understand: why do you need emergency funds?

In the time of unforeseen events, you may be in urgent need of funds. There may be a friend or family member who will lend you money for emergency purposes at times. But every time you cannot depend on others, there may be situations where your friend or family member denies giving funds. At that time, the option left is to borrow debt, which can be either borrowed through a credit card or through a personal loan. The interest rate on the borrowed amount through these two means will be very high.

It will be more difficult for the person who has an ongoing loan, and this debt will increase that person’s financial burden. Keeping these things in mind, it is necessary that you have an emergency fund saved for any unexpected events. And it also reduces your financial stress.

Okay! Now we know the reasons to have an emergency fund. But now, you may have a few questions in your mind. How do I save funds? How much emergency funds would I need? Where can I keep these funds?

Let me clear up each question one by one.

How do I save or build an emergency fund?

Saving money is harder, and spending money is very easy. Often, we have a habit of buying some products that attract us like mobile phones, watches, handbags, wallets, perfumes, etc., but later they do not add much value in life. We fall into the trap of compulsive buying. It is psychologically difficult to make a habit of saving money; one should start small.

Here are a few suggestions that may help you build an emergency fund:

1. Start saving small, rather than saving large amounts of money.

Rather than building a large corpus, which is hard and will be enough for several months, start saving money, which will be enough for a few days or a week. The habit of saving small amounts will easily help you achieve the desired savings. There is a quote saying, “Great things are done by small things brought together”. Save a small amount of money, which will become a large corpus, and the same can be used as an emergency fund.

2. Save consistently

“Consistency is the key to success.” In the same way, start saving money consistently. Don’t increase your monthly spending. Try to avoid compulsive buying or buying something that is not useful. This will help you save money consistently throughout the year.

3. Avoid credit cards and any sort of debt

When you spend through a credit card, you will not realize that you have spent any money, and when you see the bill of the card at the end of the month, you will be shocked that you have overspent. If you do not pay the credit card bill at the proper time, then you may have to pay a very high interest rate on such money. Once you get addicted to spending money through an instrument, you are very close to falling into the debt trap.

Try avoiding taking loans to buy any sort of liability (also known as assets) like a car, refrigerator, air conditioner, television, etc. Buying these things on credit will delay your savings, and you will not be able to build a fund that is required for unexpected events.

4. Monitor your savings.

Check if you can save consistently, and make note of all the spending and income and the amount you are able to save. This way, you can build your funds.

5. Only use funds during emergencies.

The emergency funds, which have been saved with a lot of difficulties, should not be spent unnecessarily. Only put hands on the account in times of true emergencies. Don’t buy unnecessary liabilities with such funds.

How much emergency funds would I need?

The size of your emergency fund is not a one-size-fits-all matter. It varies from person to person and is based on a number of variables. You can use the following important factors to estimate how much you need in your emergency fund:

1. Monthly Expenses

Your monthly expenses are one of the key components in determining the size of your emergency fund. Start by making a list of all of your regular monthly expenses, such as your rent or mortgage, utilities, groceries, insurance premiums, and travel expenses. Include discretionary spending on things like leisure and food since they might be cut during an emergency.

2. Number of Earners in the Household

Take into account the number of wage earners in your home. You might want greater emergency savings if you’re the only source of income. On the other side, if you have several income sources, you might be able to rely on one another in times of need.

3. Job Stability

The size of your emergency fund is significantly influenced by how secure your employment is. You may not require as much of a cushion as someone with a more hazardous financial situation if you have a solid job and a consistent source of income.

4. Dependents

If you have dependents, such as children or old parents, you’ll need a bigger emergency fund to account for their needs in case of an emergency. This is especially important if you’re the primary caregiver or financial provider for your dependents.

5. Health and Insurance

Consider your health and insurance coverage. If you have health issues or are underinsured, you might need a larger emergency fund to cover unexpected medical expenses. Adequate insurance can help reduce the amount you need in your fund for healthcare-related emergencies.

6. Financial Goals

Your financial objectives will also impact how much money you need for emergencies. You could need a smaller emergency fund if you’re actively saving for a particular objective, such as a home purchase or business venture, so you can put more money towards that objective.

7. Risk Tolerance

Your personal risk tolerance is an essential factor. Some people feel more secure with a larger emergency fund, while others may be comfortable with a smaller one. Your risk tolerance should align with your comfort level and financial goals.

How Much Is Enough?

Now that we’ve considered the factors that influence the size of your emergency fund, let’s discuss some general guidelines. Financial experts typically recommend having three to six months’ worth of living expenses in your emergency fund. This range provides a reasonable balance between being prepared for unexpected financial setbacks and not tying up too much of your money in a low-yield savings account.

However, it’s important to remember that these guidelines are not set in stone. Depending on your unique circumstances, you may need more or less than the suggested range.

Where can I keep these funds?

You can save it in a fixed deposit, a savings account, or certain mutual funds. These are the three easy-to-understand instruments where you can park your emergency fund. The interest on savings accounts in India is usually very low, usually around 2–4%, but you can withdraw the money whenever you need it.

In fixed deposits, the rate of interest is around 6-8%, but there will be a penalty if the money is withdrawn before maturity. Even if there is a small amount of penalty, FDs are considered the best instruments to park emergency funds. There are a few debt mutual funds that can be liquidated easily; this can also be an option to park these funds.

Conclusion

In conclusion, having an emergency fund is not just a financial recommendation; it’s a crucial lifeline for anyone striving for financial stability and peace of mind. Life is unpredictable, and unexpected expenses or emergencies can happen to anyone at any time. Without a safety net, you might find yourself in a stressful and financially precarious situation.

An emergency fund serves as your financial cushion during tough times. It allows you to cover unexpected expenses, whether it’s a medical bill, a car repair, or a sudden job loss, without resorting to high-interest loans or going into debt. Having this financial safety net in place provides you with a sense of security and reduces the anxiety that can accompany unexpected financial setbacks.